Slippage is one of the most commonly discussed concepts in crypto trading. It is usually described as an execution issue — a situation where a trade is filled at a worse price than expected, reducing profitability.

However, in arbitrage trading, slippage plays a deeper role.

It is not just a side effect of execution. It is a direct reflection of market conditions — and in many cases, it determines whether an arbitrage opportunity actually exists.

What Is Slippage in Crypto Trading

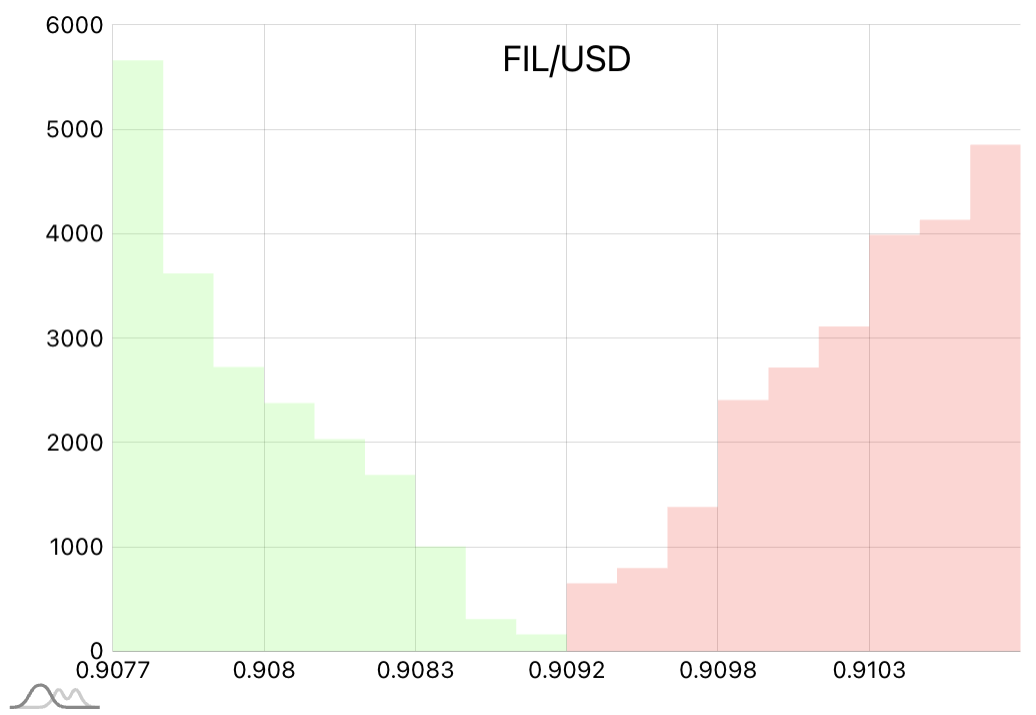

Slippage is the difference between the expected price of a trade and the actual execution price.

For example, a trader may see a price of $1.00 in the order book, but when placing an order, the trade is executed at $1.01 or higher. This difference is called slippage.

In crypto markets, slippage occurs because prices in the order book represent available liquidity across multiple levels — not a single guaranteed execution price.

Why Slippage Happens

Slippage occurs as a result of how trades interact with market liquidity. There are three key factors:

- Liquidity. Low liquidity means there is less volume available at each price level. As a result, even relatively small trades can move the price.

- Orderbook Depth. The order book consists of multiple price levels, each with its own available volume. If a trade exceeds the volume available at the best price, it moves deeper into the book.

- Trade Size. The larger the order, the more price levels it consumes. This results in a weighted average execution price that differs from the initial expectation.

Liquidity is distributed across price levels — not concentrated at a single price.

In other words, slippage is not random — it is a direct consequence of market structure.

How Slippage Affects Arbitrage

In arbitrage trading, profit margins are typically very small — often fractions of a percent. Because of this, slippage can completely eliminate expected profits.

A trade that appears profitable based on best bid/ask prices may become unprofitable once actual execution prices are taken into account. This is especially important in multi-leg arbitrage strategies, where each step introduces additional slippage and fees.

As a result, many arbitrage opportunities that look profitable in theory cannot be executed in practice.

Why Slippage Is Not Just a “Problem”

Slippage is often treated as something that needs to be minimized or avoided. But this perspective is incomplete.

Slippage is not an external issue — it is a direct consequence of how trades interact with available liquidity. If a strategy becomes unprofitable due to slippage, it means the initial price was never actually achievable at that volume.

In this sense, slippage does not break arbitrage strategies — it reveals their limitations. It exposes the gap between theoretical pricing and real execution.

How to Account for Slippage in Arbitrage

To build a sustainable arbitrage strategy, slippage must be accounted for at the evaluation stage. This involves several key principles.

First, trades should be evaluated based on weighted execution prices rather than best bid/ask values.

Second, trade size must match available liquidity to avoid excessive price impact.

Third, fees and execution structure must be included in every calculation, as they directly affect final profitability — especially when margins are small.

Finally, it is important to work with liquid markets and reliable exchanges, since liquidity determines the level of slippage and the stability of execution.

Some systems (such as HETHA) address this by modeling execution using real order book data. Instead of relying on theoretical prices, they estimate realistic outcomes before trades are placed, filtering out opportunities that are not actually executable.