Many traders evaluate arbitrage opportunities based on price differences between exchanges. A spread appears, calculations show a potential profit, and the trade seems straightforward. However, price alone does not determine profitability.

What matters is not just where the price is, but how much volume is available at that price. This is where orderbook depth becomes critical.

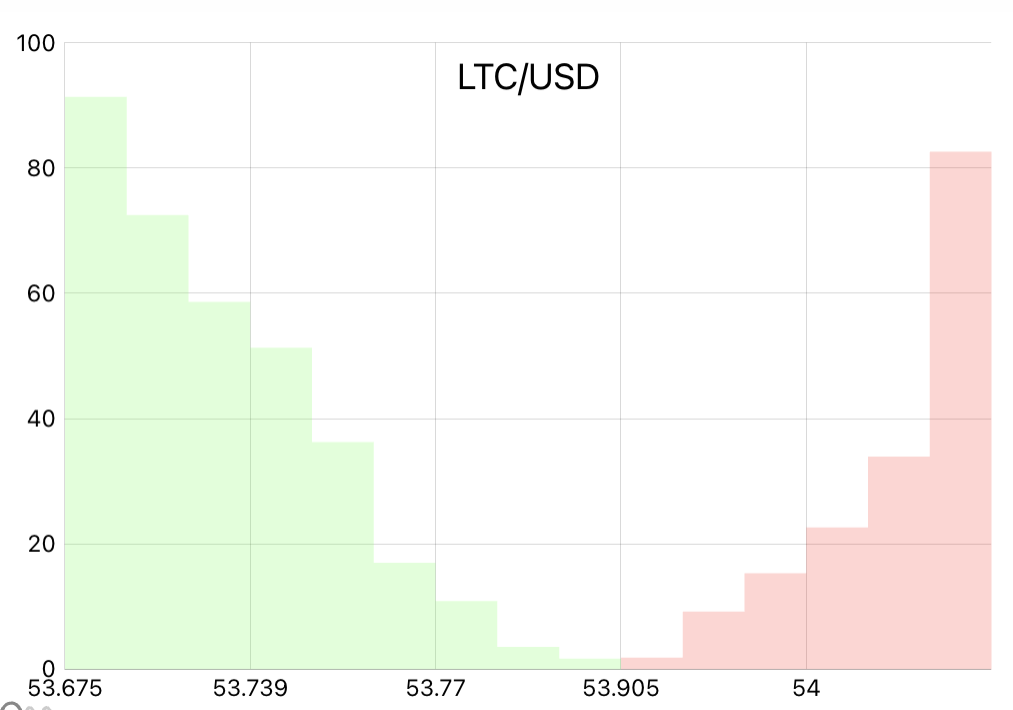

Orderbook depth is the amount of liquidity available at different price levels in the market. It defines how much volume can be executed before the price begins to change.

What Is Orderbook Depth

An orderbook is a list of buy and sell orders at different price levels. Orderbook depth refers to how much volume (liquidity) is available across these levels.

At the top of the book, you see the best bid and ask — the highest price someone is willing to buy and the lowest price someone is willing to sell. However, these prices usually represent only a small amount of volume. Beyond that, liquidity is distributed across multiple orderbook levels, each with its own price.

In practice, this means that the market is not a single price point, but a range of prices tied to available liquidity.

How Orderbook Depth Affects Execution

Execution does not happen at a single price. When a trade is placed, it consumes available liquidity from the orderbook. If the trade size exceeds the volume available at the best price, execution continues at worse levels.

Execution moves through multiple price levels as trade size increases

The deeper the orderbook needs to be accessed, the worse the effective execution price becomes. This effect is known as slippage. As a result, the larger the trade size relative to available orderbook liquidity, the further execution moves away from the expected price.

Why Price Alone Is Not Enough

A visible spread between exchanges does not guarantee profit. Most arbitrage calculations rely on top-of-book prices, assuming that trades can be executed entirely at those levels. In reality, this assumption rarely holds.

Once execution interacts with real orderbook liquidity, the effective price changes. What appears profitable at the price level may not remain profitable when volume and liquidity are taken into account.

In other words, spread does not equal profit.

Example of Execution Impact

Consider a simple arbitrage opportunity between two exchanges. At first glance:

- Buy price: 100

- Sell price: 101

- Spread: +1%

This looks profitable.

However, if only a small amount of volume is available at these prices, a larger trade will move deeper into the orderbook.

For example:

- The first portion executes at 100 → 101

- The remaining volume executes at 100.5 → 100.7

The average execution price shifts, reducing or completely eliminating the profit. The larger the trade, the stronger this effect becomes.

How Arbitrage Systems Handle This

To evaluate arbitrage correctly, systems must go beyond top-of-book prices. Instead of treating price as a fixed input, they need to model execution across the orderbook, taking into account how trades interact with available liquidity at each level, how execution price changes with trade size, and how fees and execution conditions affect the final outcome.

In HETHA.IO, arbitrage chains are evaluated using live orderbook data rather than relying only on best bid and ask prices. The system models how trades interact with liquidity and filters opportunities based on whether they remain viable under real execution conditions. As a result, the focus shifts from simply identifying spreads to understanding whether those spreads can actually be realized in practice.

Orderbook depth is a fundamental factor in crypto arbitrage. Price differences alone do not determine profitability — execution against real orderbook liquidity does. Without accounting for depth, arbitrage remains theoretical. In practice, execution defines the outcome, not price.