Understanding how an arbitrage portfolio works is essential for building a stable execution environment.

An arbitrage portfolio is not a list of coins and not simply a distribution of balances across exchanges. It is a structural configuration that determines which arbitrage chains can be constructed, recalculated, and brought to execution under live market conditions.

A portfolio does not generate profit by itself. It defines the structural boundaries within which executable chains can exist.

Liquidity as a Structural Constraint

Portfolio structure determines which trading pairs the system can operate on. If the portfolio consists primarily of assets connected to low-liquidity markets, the constructed chains will depend on weak order books.

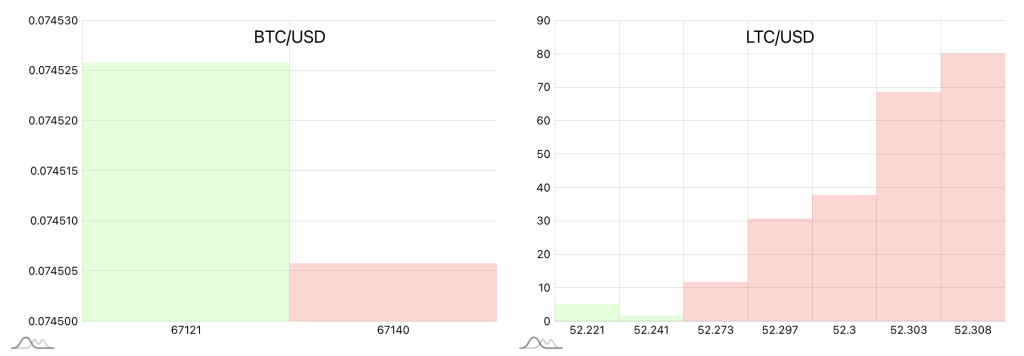

Pairs with deeper order books break less often during recalculation, remain more stable under market updates, and allow a larger number of chains to survive until execution.

Low liquidity does not automatically make a chain unprofitable at the calculation stage. However, during execution, insufficient market depth may lead to price slippage, partial volume closure, or failure at one of the route steps.

Comparison of order book depth

Used Assets vs Total Balance

In an arbitrage portfolio, the key variable is not total balance, but which assets actually participate in chain construction. If an asset is present in the portfolio but does not appear in executable routes, it does not influence the arbitrage result. It does not participate in recalculation or execution.

Portfolio size and portfolio structure are not the same. Only the structural component affects execution.

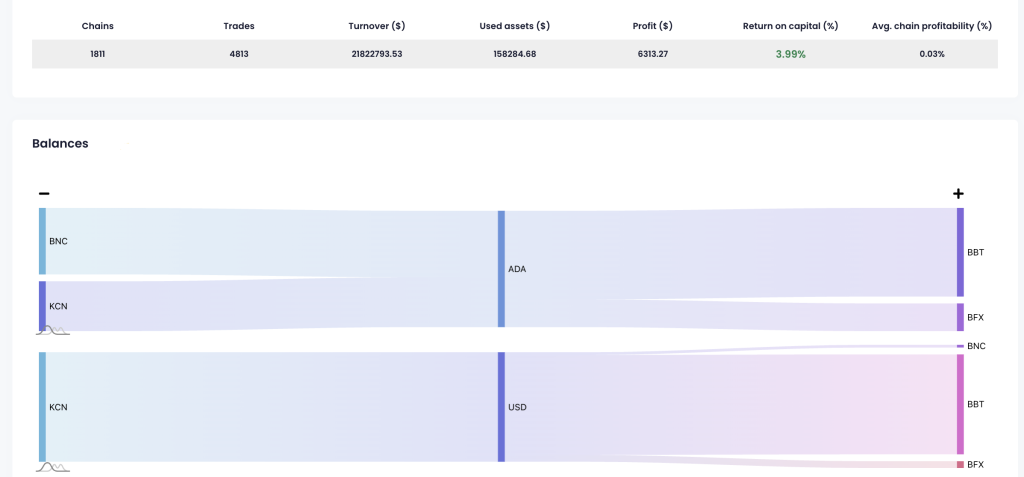

Moneyflow view showing assets participating in execution

Base Currency Alignment

Chains are constructed relative to a base currency (USDT / BTC). Portfolio assets must align with this structure.

If assets do not connect efficiently to the base currency or do not form stable chain paths, they drop out during recalculation due to execution constraints. The system does not reject them arbitrarily — they simply fail to produce executable chains.

Base currency alignment determines whether assets can participate in executable routes at all.

Chain construction relative to a base currency

Nominal vs Real Profit

Nominal profit appears at the chain calculation stage. It is derived from current order books and calculation rules. Without positive nominal profit, a chain cannot proceed further in the system. Real profit appears only after execution.

The gap between them exists because the market continues to update and execution conditions may change before completion.

Nominal profit answers the question:

“Is this chain structurally viable right now?”

Real profit answers:

“What was actually realized after execution?”

Conclusion

An arbitrage portfolio is not a set of assets, but a system of constraints. It determines which markets the system can operate on, which assets participate in chain construction, whether they align with the base currency structure, and which calculated chains have a realistic chance of reaching execution. For this reason, arbitrage results depend not on balance size, but on how structurally compatible the portfolio is with the live market environment.